Profiling and Risk in Investing

Profiling helps both the investor and the fund advisor make decisions related to the investment pie and how much money can be invested in high, medium or low risk return investments.

How much risk can you take?

This depends on not only being ready to take high risk but having the ability in terms of the funds to take the loses if they may arise. Just your ability to take risk doesn’t mean you should.

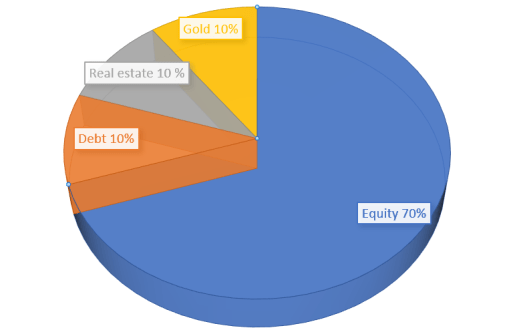

If you can take high amounts of risk, that could mean you are ready to invest more in equity than debt. Note, high risk means 70% equity and 30% debt whereas low risk is the converse – 30% equity and 70% debt. Here high risk does not mean 100% equity or low risk does not mean 100% debt.

But it is not always the case that a high-risk investment can result in more income. Rather a high risk and low risk asset allocation can sometimes end up with rather similar results. That why you will find disclaimers on nearly all pages that talk about investing, say, in mutual funds.

THE STRATEGY OF PROFILING

Basics steps in profiling include risk profiling, asset allocation and portfolio construction.

01

Risk Profiling

Here you must ask yourself questions such as how much risk you can take versus what your mindset for risk is. Questions related to total annual income, savings, future actions and acceptable loses are part of risk profiling.

02

Asset Allocation

According to the risk profiling done above, the ratio of investment classes can then be decided. The first investment pie is less risky than the second investment pie.

03

Portfolio Construction

According to the asset allocation, schemes and options can be considered.

Example – My risk profile may tell me I have a high capacity for risk and a moderate level of tolerance. It may tell me that such “investors are looking for moderate to high capital growth over a longer term; cautious towards taking high levels of risk, however comfortable with short term fluctuation in returns”. According to this I may be suggested a 60% debt 40% equity investment of my capital. So now I look for specific debt funds, dividing this according to the capital amount, and look for different equity schemes such as blue-chip shares or general equity shares. Further you may decide to have a one-time lump sum investment or choose to invest in a systematic investment plan (SIP) weekly, monthly, or periodical investment at your choice.

For an investment pie having equity at 40% and debt at 60% this could be the asset allocation details for a person with a balanced risk profile:

Disclaimer: The contents of this page do not constitute investment advice. Please contact your authorised investment advisor before making any investments or acting upon the contents of this page.